.jpg)

If you even want the option to retire in your 50s, and your entire plan is “I’ll just max out my 401(k),” it’s probably time to reassess your strategy.

That’s not a knock. Only about 14% of Americans max out their 401(k) each year. If you’re doing that consistently, you’re already ahead of the curve and building a strong foundation.

But for many high-earning professionals, that foundation quietly becomes the entire plan. And that’s where early retirement flexibility often breaks down.

The Problem With Relying Too Heavily on a 401(k)

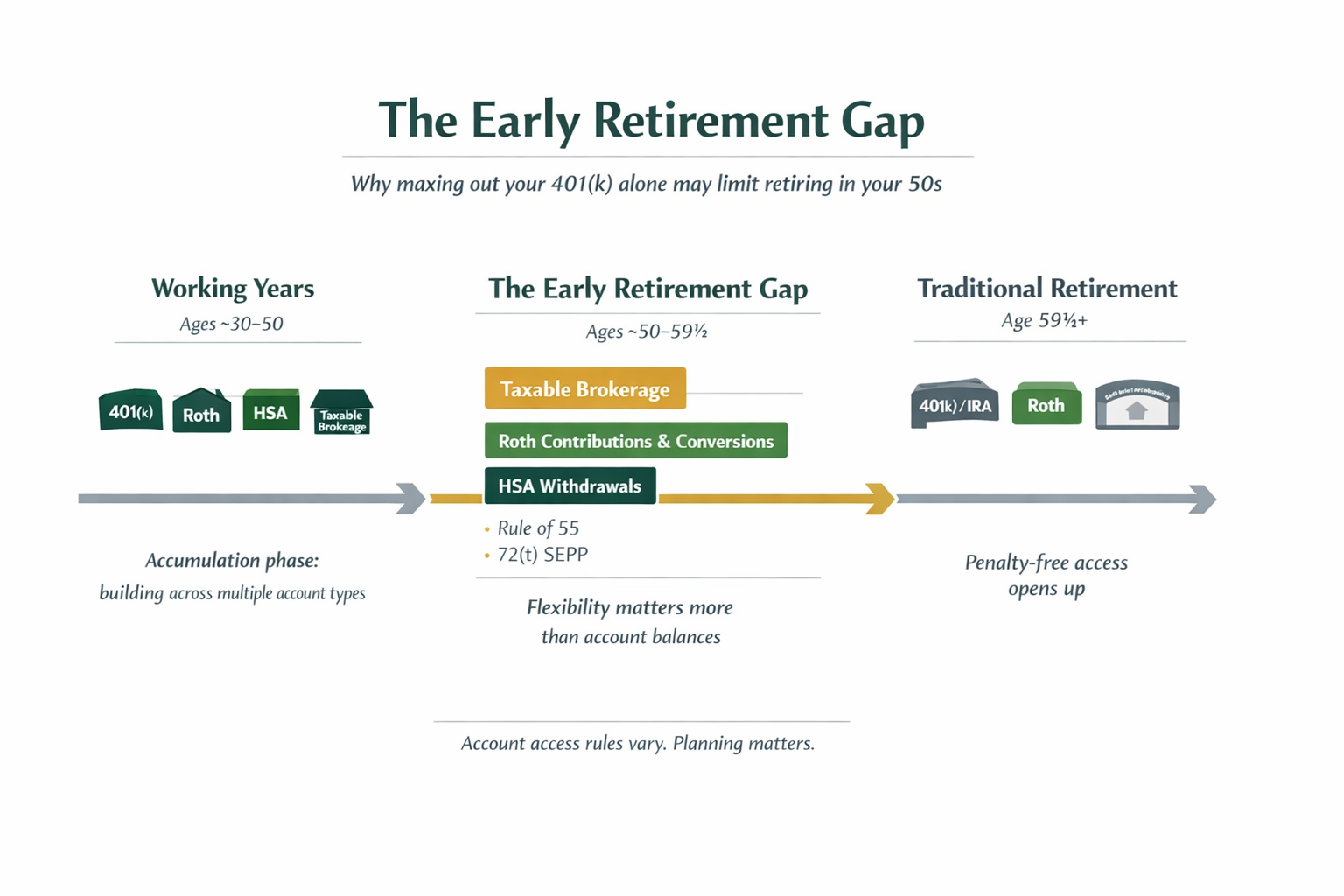

401(k)s and other tax-deferred retirement accounts are designed for traditional retirement timing. Most funds aren’t accessible penalty-free until age 59½.

When 90% or more of your investment assets live inside these accounts, retiring early becomes much harder in practice. You may have a healthy net worth on paper but limited flexibility in real life.

Yes, there are ways to access retirement funds early—but each comes with trade-offs.

The Rule of 55: A Useful Tool With Narrow Application

One commonly referenced option is the Rule of 55. This allows penalty-free withdrawals from your current employer’s 401(k) if you separate from service in the year you turn 55 or later.

While helpful in the right situation, the Rule of 55 has limitations:

- It applies only to the 401(k) of the employer you separate from

- It does not apply to IRAs or old 401(k) plans

- Withdrawals are still taxed as ordinary income

- Employer plan rules can restrict withdrawal flexibility

For some individuals, the Rule of 55 can serve as a partial bridge. For others, the timing and constraints make it unreliable as a primary early-retirement strategy.

72(t) Distributions: Access Without Flexibility

Another option is 72(t) distributions, also known as Substantially Equal Periodic Payments.

These allow penalty-free access before age 59½, but they come with significant restrictions:

- You must take the same calculated withdrawal each year

- Payments must continue for at least five years or until age 59½, whichever is longer

- Changes or errors can trigger penalties retroactively

- There is no flexibility for market conditions or lifestyle changes

This rigidity can be especially challenging for those trying to bridge the gap between their early 50s and traditional retirement age.

Why Taxable Brokerage Accounts Are Critical for Early Retirement

This is where taxable brokerage accounts play a much larger role than most people realize.

A well-managed taxable account provides:

- Access to funds at any age

- No required minimum distributions

- No contribution limits

- Greater control over tax timing

Unlike retirement accounts, taxable brokerage accounts allow you to decide when gains are realized. Long-term capital gains are often taxed at lower rates than ordinary income, and early retirement years may present opportunities for highly efficient tax planning.

Taxable accounts also create real flexibility. They can help:

- Bridge income before retirement accounts are accessible

- Manage cash flow during market downturns

- Delay Social Security strategically

- Reduce reliance on rigid early-withdrawal rules

Used intentionally, taxable brokerage accounts often become the backbone of a successful early retirement plan.

The Key Pillars of an Early Retirement Strategy

Early retirement isn’t just about saving more—it’s about diversifying where your savings live.

Some of the most effective pillars include:

Taxable Brokerage Accounts

Provide liquidity, flexibility, and tax planning opportunities before traditional retirement age.

Roth Accounts

Offer tax-free growth and withdrawals, helping manage future tax brackets and long-term flexibility.

Health Savings Accounts (HSAs)

When invested and used strategically, HSAs can function as a powerful supplemental retirement account, especially before Medicare eligibility.

Intentional Plan Design

The most important pillar of all. Coordinating account types, withdrawal timing, and tax strategy matters far more than maximizing any single account in isolation.

The Bottom Line

Maxing out your 401(k) is a great foundation and should absolutely be part of a long-term retirement strategy.

But if retiring in your 50s is even a possibility you want to keep open, it shouldn’t be the only pillar of your plan. A strategy built entirely around tax-deferred accounts may look strong on paper but feel restrictive in practice.

The goal isn’t to save blindly—it’s to build a plan that supports the life you want, on the timeline you want.

Starting earlier gives you more options. Waiting too long often removes them.

Compliance Disclosure

This content is for informational and educational purposes only and does not constitute investment, tax, or legal advice. Individual circumstances vary, and strategies discussed may not be appropriate for all investors. Please consult with a qualified financial professional and tax advisor before implementing any planning strategies.

.png)

.png)